“Eendragt Maakt Magt” – Investing in Mutual Funds

- Vibhav Bhat and Yash Bhave

- Jun 6, 2021

- 5 min read

Updated: Jun 7, 2021

Written By- Vibhav Bhat and Yash Bhave

PGDM Students, TAPMI- Manipal

It all started in 1774 when Adriaan van Kewitch, a Dutch merchant, formed an investment trust pooling money together. “Eendragt Maakt Magt” (Unity creates strength) fund allowed investors to purchase limited shares and were backed by income from plantations. This was the first seed which would later bloom into modern day mutual funds as we know today.

What are Mutual Funds?

A mutual fund is a professionally managed investment fund. It pools money from a group of investors and invests this pool in securities including stocks, bonds, options, futures, currency treasuries and money market securities.

Modern day mutual funds have various classifications based on criteria. SEBI in Oct 2017 categorized mutual funds and behaviors to give a rational idea to investors. Majorly it can be classified as an equity fund, debt fund or a hybrid fund.

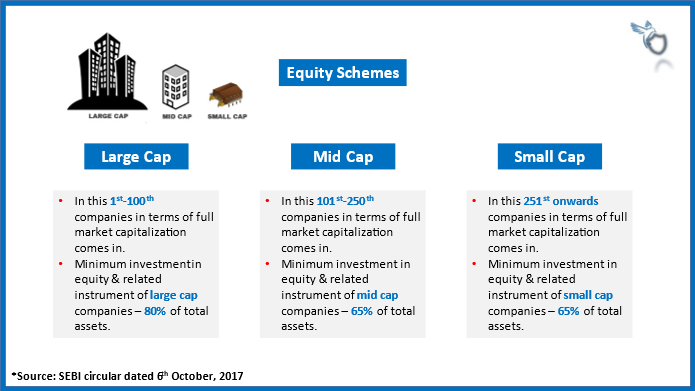

Another classification as per the SEBI circular defines funds as large, mid, small, or Flexi-cap funds. Each AMC can have only one fund for each of these categories.

Apart from these classifications, a mutual fund can also be classified as active or passive funds. There also exist Equity-linked savings schemes (ELSS) which have to follow laws set by the government.

“Mutual Funds sahi hai”- but why?

We all have seen ads that say “Mutual funds sahi hai” but it does not say why. Traditionally Indians have opted for investments such as FD, RD, PPF and others that guarantee fixed return and security. In sharp contrast the returns on any mutual fund are not fixed and have higher risk.

Fig- Mutual Fund returns against respective benchmarks

Source: Money control (https://www.moneycontrol.com/)

Unlike Laxmi Chit fund investors, there existed a fear among the populace regarding the safety of the money being invested in these funds. However, if we compare returns for good funds, we can see that they are able to beat the market index benchmarks and provide good returns with diversified risk within the pool as seen in figures. Overtime this fear has reduced. As such selection of the fund becomes a quintessential ingredient in the recipe.

Which fund is right for you?

Selecting a mutual fund for individual investors is a lone wolf task. Prior to investing one needs to decide the goal/reason for investment. Once the goal is finalized it has to be converted in financial terms. A goal can be buying a car 5 years down the line. The car can be worth 10 Lakhs.

The choice of funds is individual responsibility. You can either choose Equity, Debt or hybrid in your portfolio. Hybrid funds are usually preferred because of lower risks combined with better returns. It also depends on the point you are in your life cycle. As per fund managers and analysts, youngsters can have 30% of debt fund and 70% as equity fund whereas for the senior citizen 40% as Equity fund and 60% as debt fund.

A simple explanation for this is the consequences of risk at that stage of life. A youngster can bear more loss and still continue his way of living because of a stable source of income whereas senior citizens (who are usually retired and do not have stable source of income) cannot bear higher loss on their life savings.

How do you select the fund?

First step is selecting the type of fund for your portfolio. It can be bluechip, mid, small or flexicap depending on your goal.

The second step in fund selection is selecting the right AMCs. There are a significant number of AMCs out there but selecting the right one is the most important task. Research the background of AMC including their fund managers, CIO and Head of Research. These are the individuals who will be dealing with your money and should have a strong background with experience, responsibility and most importantly proved credible results.

Third step is researching the historical returns of identified funds and if the return predictions are appropriate for your goal. The returns have to be analyzed against category average and benchmarks. Make sure your research is extensive and includes more than 1 opinion about the fund's future.

Fourth step is to cross verify the past returns with the fund manager's history. If a fund manager exists for 3 years managing the fund, check the returns for the past 3 years. It will give you a rough understanding of the impact the fund manager has on fund returns.

A major aspect while following these basic steps is to understand that these are not exhaustive or absolute. It has to be analyzed with an open view of macroscopic factors as well for deducing reasons on fund performance.

Fifth step is determining the method of investment. You can either invest in lump-sum amounts trying to time the market or make a Systematic investment plan (SIP). A SIP usually involves monthly fixed investments in the fund. It has been recorded that SIP usually outperforms attempts to time the lumpsum investments. It also reduces the burden of investment by spreading it evenly across the year.

Based on our research, currently good funds include- Kotak Mahindra Flexi-cap Fund, Mirae asset large-cap fund (Emerging Bluechip) , Axis Blue Chip, Parag Parikh Long term equity fund, Axis mid-cap, SBI small-cap, and SBI equity hybrid fund.

(Please note this is based on our point of view and by no way an indication for best AMCs for investment)

Investment Apps - pros and cons

An emerging trend can be seen with investors opting to go through an investment app as one stop solution for their investment needs and research. These apps have made the life of investors very easy by facilitating various features at fingertips like, buy, sell, switch scheme, and many other things.

Fig - Investment Apps available in market

With people getting comfortable with technology and ever increasing internet penetration this trend is predicted to increase over time. Once the KYC (Know Your Customer) step is done then the transaction barely takes a few minutes. Another benefit is that it is paperless and can be done from any place. It saves a lot of time for investors. It is also easier to monitor progress of investment over a period. It acts as one stop investment solution for new investors which get accustomed to it over time.

On the other hand generalized services are offered and not much customization is available as per the need of an investor. They also lack detailed research on the funds hence, it is always advisable that investors do their research and then take investment calls. Also, data security issues arise as investors have to give a lot of personal data to the application. Investors face a major threat in case investment and portfolio data is leaked.

25 din me paisa double can happen only in lottery. Investment in Mutual fund on other hand will reward patience. In current scenario the returns on all securities have showed high volatility. However, in long run investing in the right mutual fund can be rewarding. Overall we can still say "Mutual Funds Sahi Hai"

Comments